Outright Monetary Transactions

&

Quantitative Easing

Combined Weapons of Fiscal Mass-Destruction

Like our sister organization the EZB the EOZB takes its main task of stabilising the

euro's purchasing power and thus price stability in the European Union very

seriously. Therefore our Stability-Division is greatly concerned since Mario Draghi

said last year just one word “Unlimited”! From this day on the EZB was ready to buy

unlimited quantities of government bonds from the euro-zone countries if they

requested aid from the European Stability Mechanism thus triggering jubilation in the

financial markets.

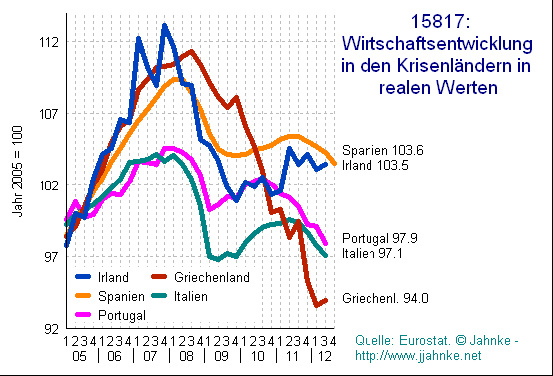

At first sight the Outright-Monetary-Transactions policy was successful via

stabilizing the interest rates of the government bonds but at second sight it will pave

the way into an European crises affecting us the people of Europe. If we want to

know why we have to take look at the following graph showing the economic

development of the indebted countries:

&

Quantitative Easing

Combined Weapons of Fiscal Mass-Destruction

Like our sister organization the EZB the EOZB takes its main task of stabilising the

euro's purchasing power and thus price stability in the European Union very

seriously. Therefore our Stability-Division is greatly concerned since Mario Draghi

said last year just one word “Unlimited”! From this day on the EZB was ready to buy

unlimited quantities of government bonds from the euro-zone countries if they

requested aid from the European Stability Mechanism thus triggering jubilation in the

financial markets.

At first sight the Outright-Monetary-Transactions policy was successful via

stabilizing the interest rates of the government bonds but at second sight it will pave

the way into an European crises affecting us the people of Europe. If we want to

know why we have to take look at the following graph showing the economic

development of the indebted countries:

The recession is the direct consequence of the austerity measures of the Troika on

the indebted countries in Europe. Instead of reducing the debts of these countries the

ever faster unfolding economic downturn is leading to higher debt ratios despite the

austerity policies implemented on the countries thus defying economical lore to the

core! If the recession goes on there will come the point when the bond holders will

lose their trust in them. Quite the opposite we can observe in Island where the

creditors had to pay. Here a question arises: Did Draghi really study economics? Or

do we have here another case of Gutenberg? We will know soon. A team of our

Quality-Management-Division is already on the task – thanks to Google it will be

easy to prove!

To make things worse we can observe the ongoing policy of qualitative easing of

the ECB resulting in cheap money flooding the financial markets like nothing was

amiss. Last October we evaluated a plus of 3,9% of the money supply M3 while

economic growth in the euro zone was going negative hence representing the illness

of modern central banking policies. If Draghi knows some economics he should be

aware of the logical consequence of a money supply outstripping economic growth –

inflation!

Luckily macro-economics is far more simple than economists wants us to believe.

Therefore we have a question to the chief economist of the ECB: What will happen

when the financial markets loose their trust in the government bonds of the indebted

countries while OMT is ready for action? The bondholders will sell their bonds which

will be bought by the ECB in unlimited quantities holding the banks in business and

thus creating liquidity. At the same time the ECB will flood the European markets

which cheap credits enabling the banks to buy what can be bought in the real world

resulting into an even faster enfolding inflation in the euro-zone? What will be the

outcome of this scenario?

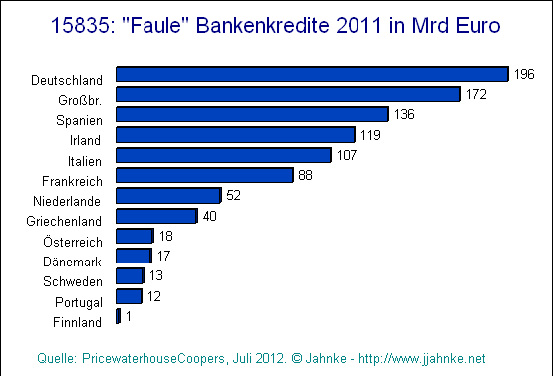

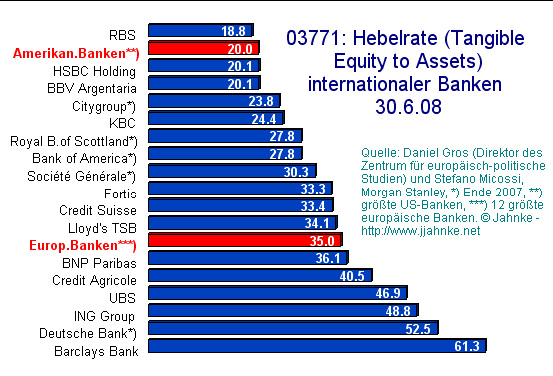

To understand what will happen we take a look at these two graphs. The first shows

the bad credits of European banks. The second shows the leverage ratio of

international banks:

the indebted countries in Europe. Instead of reducing the debts of these countries the

ever faster unfolding economic downturn is leading to higher debt ratios despite the

austerity policies implemented on the countries thus defying economical lore to the

core! If the recession goes on there will come the point when the bond holders will

lose their trust in them. Quite the opposite we can observe in Island where the

creditors had to pay. Here a question arises: Did Draghi really study economics? Or

do we have here another case of Gutenberg? We will know soon. A team of our

Quality-Management-Division is already on the task – thanks to Google it will be

easy to prove!

To make things worse we can observe the ongoing policy of qualitative easing of

the ECB resulting in cheap money flooding the financial markets like nothing was

amiss. Last October we evaluated a plus of 3,9% of the money supply M3 while

economic growth in the euro zone was going negative hence representing the illness

of modern central banking policies. If Draghi knows some economics he should be

aware of the logical consequence of a money supply outstripping economic growth –

inflation!

Luckily macro-economics is far more simple than economists wants us to believe.

Therefore we have a question to the chief economist of the ECB: What will happen

when the financial markets loose their trust in the government bonds of the indebted

countries while OMT is ready for action? The bondholders will sell their bonds which

will be bought by the ECB in unlimited quantities holding the banks in business and

thus creating liquidity. At the same time the ECB will flood the European markets

which cheap credits enabling the banks to buy what can be bought in the real world

resulting into an even faster enfolding inflation in the euro-zone? What will be the

outcome of this scenario?

To understand what will happen we take a look at these two graphs. The first shows

the bad credits of European banks. The second shows the leverage ratio of

international banks:

|

|

Truth to tell the European banks are more or less insolvent kept afloat by the cheap

money of the ECB. When the European economics will start to disintegrate they will

implode. Now comes the ESM into play which is designed to rescue the big banks in

case of emergency. The outcome will be small banks going Bankruptcy in the

thousands (The difference of the US compared to Europe – it already happened on a

small scale) while the big institutes will be rescued resulting in the biggest market

consolidation in the history of our banking system and Anus Jains words in his

speech to his staff when he became CEO of the German Bank will come true: only 5

will be left! All the while the people of Europe will experience the biggest

economical crises in their history! At this point we advice our sister institute the ECB

to remember its independence and follow the lead of Island and letting the Banks go

insolvent while saving the money of us the people!

money of the ECB. When the European economics will start to disintegrate they will

implode. Now comes the ESM into play which is designed to rescue the big banks in

case of emergency. The outcome will be small banks going Bankruptcy in the

thousands (The difference of the US compared to Europe – it already happened on a

small scale) while the big institutes will be rescued resulting in the biggest market

consolidation in the history of our banking system and Anus Jains words in his

speech to his staff when he became CEO of the German Bank will come true: only 5

will be left! All the while the people of Europe will experience the biggest

economical crises in their history! At this point we advice our sister institute the ECB

to remember its independence and follow the lead of Island and letting the Banks go

insolvent while saving the money of us the people!